Medicare Advantage vs. Original Medicare 2026: Your Definitive Guide

Medicare Advantage vs. Original Medicare 2026: A Data-Backed Comparison for Your Health Coverage Decisions

Navigating the complex world of Medicare can feel like deciphering a foreign language, especially when contemplating your health coverage options for the upcoming year. As we look ahead to 2026, understanding the fundamental differences between Medicare Advantage (Part C) and Original Medicare (Parts A and B) is more crucial than ever. This comprehensive guide aims to demystify these choices, providing you with a data-backed comparison to empower your health coverage decisions. Our focus keyword, Medicare 2026 Comparison, will guide us through the nuances of each option, ensuring you have the insights needed to select the plan that best suits your individual needs and lifestyle.

The landscape of healthcare is constantly evolving, and Medicare is no exception. Annual changes, driven by legislative updates, economic factors, and shifts in healthcare needs, mean that what was true last year might not hold for 2026. Therefore, a proactive approach to understanding your options is paramount. While both Medicare Advantage and Original Medicare provide essential health coverage for millions of Americans aged 65 and older, or those with certain disabilities, their structures, costs, benefits, and flexibility vary significantly. Making an informed decision now can have a profound impact on your access to care, out-of-pocket expenses, and overall peace of mind in the years to come.

Understanding Original Medicare: The Foundation of Coverage

Original Medicare, established in 1965, is the traditional fee-for-service program offered directly by the federal government. It consists of two main parts:

- Part A (Hospital Insurance): Covers inpatient hospital stays, skilled nursing facility care, hospice care, and some home health care. Most people don’t pay a monthly premium for Part A if they or their spouse paid Medicare taxes through employment for a specified period (typically 10 years or 40 quarters).

- Part B (Medical Insurance): Covers certain doctors’ services, outpatient care, medical supplies, and preventive services. Everyone pays a monthly premium for Part B, which is typically deducted from their Social Security benefits. The standard Part B premium for 2026 will be announced later, but it’s important to budget for this expense.

Key Features and Considerations for Original Medicare in 2026:

- Nationwide Acceptance: One of the most significant advantages of Original Medicare is its wide acceptance. You can see any doctor, specialist, or hospital in the U.S. that accepts Medicare, without needing a referral. This offers unparalleled flexibility, especially for those who travel frequently or live in different states throughout the year.

- Cost-Sharing: Original Medicare has deductibles, copayments, and coinsurance that beneficiaries are responsible for. For instance, after meeting your Part B deductible, you typically pay 20% of the Medicare-approved amount for most doctor services and outpatient therapy. There is no annual out-of-pocket maximum with Original Medicare, which can lead to substantial expenses in the event of serious illness or chronic conditions.

- Prescription Drug Coverage (Part D): Original Medicare does not include prescription drug coverage. To get this, you would need to enroll in a separate Medicare Part D Prescription Drug Plan (PDP). These plans are offered by private insurance companies approved by Medicare.

- Medigap (Medicare Supplement Insurance): To help cover the out-of-pocket costs associated with Original Medicare (like deductibles, copayments, and coinsurance), many beneficiaries purchase a Medigap policy. These policies are sold by private insurance companies and can significantly reduce your financial exposure. However, Medigap policies come with their own monthly premiums, which vary based on the plan, your age, and your location. It’s crucial to note that you cannot have a Medigap policy if you are enrolled in a Medicare Advantage plan.

- No Referral Required: With Original Medicare, you generally don’t need a referral from a primary care doctor to see a specialist, providing direct access to the care you need.

For Medicare 2026 Comparison, understanding the baseline provided by Original Medicare is essential before delving into its alternative. The freedom of choice of providers and the ability to combine it with a Medigap policy for more predictable out-of-pocket costs are often cited as its primary benefits. However, the lack of an out-of-pocket maximum and the need for separate drug coverage are significant considerations.

Exploring Medicare Advantage (Part C): An All-in-One Alternative

Medicare Advantage plans are offered by private insurance companies approved by Medicare. These plans provide all the benefits and services covered by Original Medicare (Part A and Part B), and often include additional benefits that Original Medicare does not cover. Think of Medicare Advantage as an ‘all-in-one’ alternative to Original Medicare.

Key Features and Considerations for Medicare Advantage in 2026:

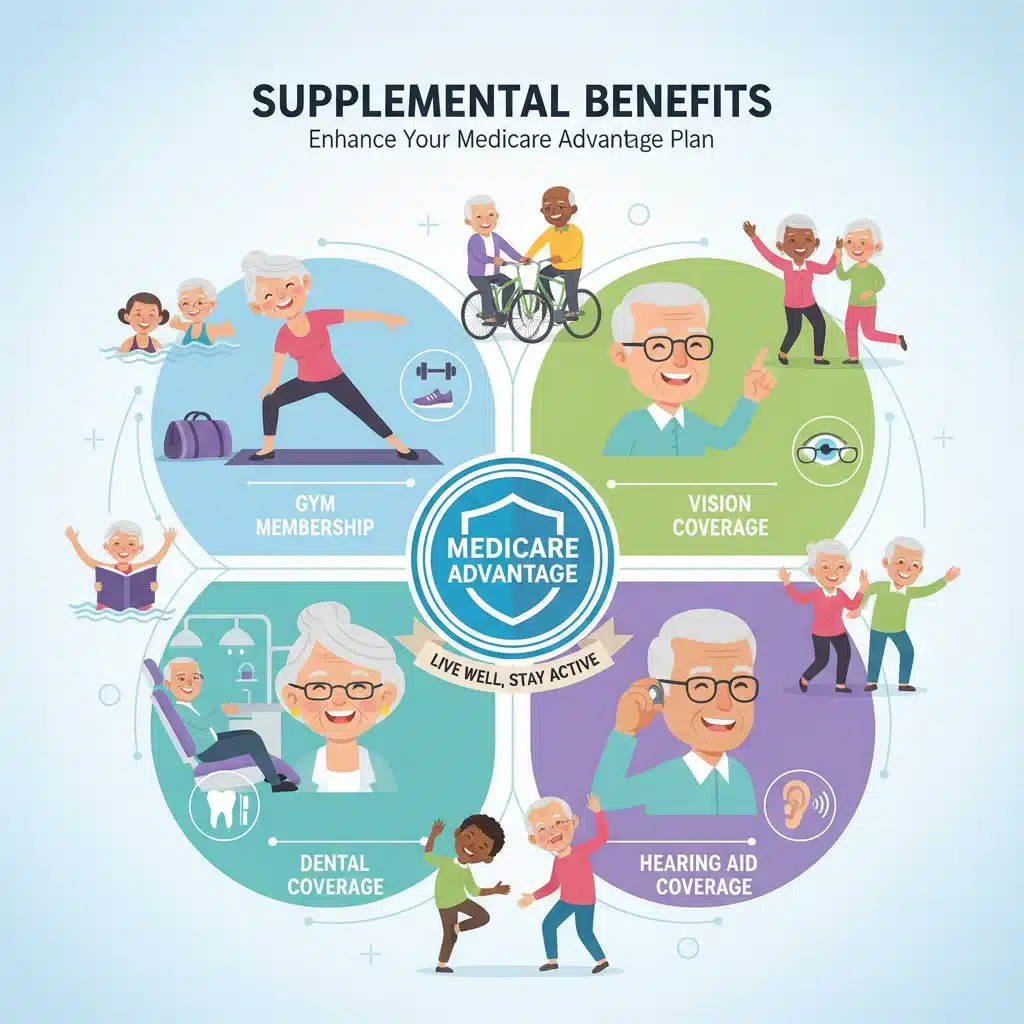

- Bundled Benefits: Medicare Advantage plans typically bundle Part A, Part B, and usually Part D (prescription drug coverage) into one comprehensive plan. Many plans also offer extra benefits such as vision, hearing, dental, and wellness programs (like gym memberships), which are not covered by Original Medicare.

- Network Restrictions: Most Medicare Advantage plans operate with networks of doctors, specialists, and hospitals. This means you may need to choose providers within the plan’s network, or pay more if you go out-of-network (depending on the plan type, such as HMO or PPO). Referrals may also be required to see specialists. This is a significant difference when considering Medicare 2026 Comparison.

- Out-of-Pocket Maximum: A major benefit of Medicare Advantage plans is that they have an annual out-of-pocket maximum. Once you reach this limit, the plan pays 100% of your covered healthcare costs for the rest of the year. This provides a crucial financial safety net that Original Medicare lacks.

- Monthly Premiums: While you must continue to pay your Part B premium, many Medicare Advantage plans have low or even $0 additional monthly premiums. However, lower premiums often come with higher deductibles, copayments, or coinsurance for services.

- Plan Types: Common types of Medicare Advantage plans include Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), Private Fee-for-Service (PFFS) plans, and Special Needs Plans (SNPs). Each type has different rules about how you get services and how much you pay.

For those prioritizing bundled services, additional benefits, and a cap on out-of-pocket expenses, Medicare Advantage can be a very attractive option. However, the potential for network restrictions and the need for referrals are important trade-offs to consider. The variety of plans available means that careful research is needed to find a plan that aligns with your specific health needs and preferences.

Medicare 2026 Comparison: Costs and Coverage Breakdown

Let’s delve deeper into a direct comparison of costs and coverage for Medicare 2026 Comparison. This section will highlight the financial implications and service access differences between the two options.

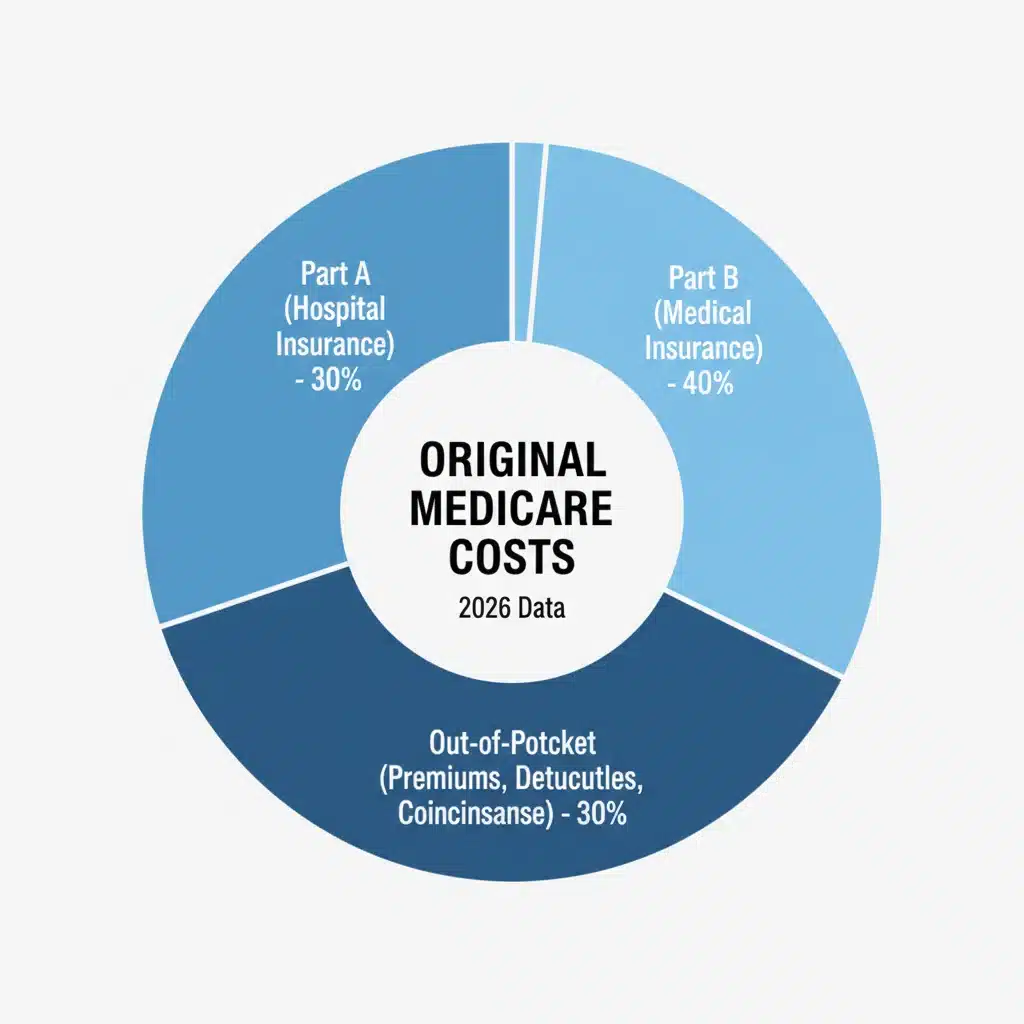

Cost Structures:

- Original Medicare:

- Part A Premium: $0 for most beneficiaries.

- Part B Premium: Standard monthly premium (to be announced for 2026).

- Part A Deductible: Inpatient hospital deductible per benefit period (to be announced for 2026).

- Part B Deductible: Annual deductible (to be announced for 2026). After deductible, 20% coinsurance for most services.

- No Out-of-Pocket Maximum: This is a critical point. Without a Medigap plan, your 20% coinsurance can accumulate indefinitely.

- Medigap Premiums: Additional monthly premiums if you choose to purchase a Medigap policy.

- Part D Premiums: Additional monthly premiums for a stand-alone Prescription Drug Plan.

- Medicare Advantage:

- Part A Premium: $0 for most beneficiaries (you still qualify for Part A).

- Part B Premium: You must continue to pay your Part B premium to the government.

- Plan Premium: Many plans have a $0 additional monthly premium, while others may have a small premium.

- Deductibles, Copayments, Coinsurance: Varies significantly by plan. You will have specific copayments for doctor visits, hospital stays, and other services.

- Out-of-Pocket Maximum: All Medicare Advantage plans have an annual out-of-pocket maximum. For 2026, this limit will be set by CMS, offering financial protection against catastrophic costs.

- Part D Included: Most plans include prescription drug coverage, eliminating the need for a separate Part D plan premium.

Coverage and Flexibility:

- Original Medicare:

- Provider Choice: Freedom to choose any doctor, specialist, or hospital nationwide that accepts Medicare.

- Referrals: Generally not required for specialists.

- Additional Benefits: Does not cover routine vision, dental, hearing, or wellness programs. These would need to be paid out-of-pocket or through separate private insurance.

- Medicare Advantage:

- Provider Choice: Typically restricted to a network of providers (HMOs) or offers lower costs for in-network providers (PPOs). Out-of-network care may be limited or more expensive.

- Referrals: Often required for specialists in HMO plans.

- Additional Benefits: Frequently includes vision, dental, hearing, and fitness benefits, providing a more comprehensive package.

When conducting your Medicare 2026 Comparison, consider your anticipated healthcare utilization. If you value broad access to specialists across the country and don’t mind managing separate policies (Medigap and Part D), Original Medicare might be appealing. If you prefer an all-in-one plan with predictable out-of-pocket costs and value additional benefits, even with network restrictions, Medicare Advantage could be a better fit.

Data Trends and Projections for 2026

Looking at historical data and current trends can provide valuable insights for your Medicare 2026 Comparison. The Centers for Medicare & Medicaid Services (CMS) continually analyzes and updates Medicare policies and offerings.

Growth of Medicare Advantage:

Medicare Advantage enrollment has been steadily increasing. According to CMS data, nearly half of all Medicare beneficiaries are now enrolled in a Medicare Advantage plan. This trend is expected to continue into 2026, driven by several factors:

- Attractive Additional Benefits: The inclusion of vision, dental, hearing, and wellness programs is a significant draw for many seniors.

- Low or $0 Premiums: The perception of lower monthly costs compared to Original Medicare plus Medigap and Part D is a powerful incentive.

- Out-of-Pocket Maximum: The financial security provided by an annual out-of-pocket limit is highly valued, especially given rising healthcare costs.

- Targeted Plans: The availability of Special Needs Plans (SNPs) tailored to individuals with specific chronic conditions or financial needs makes Medicare Advantage a suitable option for a diverse group of beneficiaries.

Original Medicare Stability:

While Medicare Advantage grows, Original Medicare remains the bedrock of the system. It continues to provide consistent, broad coverage without network limitations. For some beneficiaries, particularly those with complex or rare conditions requiring highly specialized care from specific providers, Original Medicare with a Medigap plan offers the peace of mind of unrestricted access to care.

Potential Changes for 2026:

While specific details for 2026 premium and deductible amounts are yet to be finalized, beneficiaries should anticipate modest increases in Part B premiums and deductibles, consistent with historical trends driven by healthcare inflation. Medicare Advantage plans will likely continue to offer a wide array of options, with insurers competing to provide appealing benefit packages. It’s crucial to review the Annual Notice of Change (ANOC) and Evidence of Coverage (EOC) documents each fall to understand the specifics of your plan for the upcoming year.

When making your Medicare 2026 Comparison, consider these trends and how they align with your personal healthcare philosophy and financial planning. The increasing popularity of Medicare Advantage indicates a shift towards managed care for many, but the enduring strength of Original Medicare highlights its continued relevance for others.

Making Your Decision: Factors to Consider for Medicare 2026 Comparison

Choosing between Medicare Advantage and Original Medicare is a highly personal decision. There’s no one-size-fits-all answer. Here are key factors to weigh when conducting your Medicare 2026 Comparison:

1. Your Health Status and Healthcare Needs:

- Healthy and Active: If you’re relatively healthy and primarily need preventive care, a Medicare Advantage plan with a low or $0 premium and extra benefits like gym memberships might be very attractive.

- Chronic Conditions or Frequent Doctor Visits: If you have chronic conditions, require frequent specialist visits, or anticipate significant medical needs, consider the cost-sharing structure. An Original Medicare plan with a comprehensive Medigap policy might offer lower overall out-of-pocket costs in the long run, despite higher monthly premiums. Conversely, a Medicare Advantage plan with a low out-of-pocket maximum could also be beneficial, provided your preferred doctors are in-network.

- Prescription Drug Needs: Do you take many prescriptions? Most Medicare Advantage plans include Part D, simplifying your coverage. With Original Medicare, you’ll need a separate Part D plan, and you’ll need to compare formularies and costs carefully.

2. Financial Situation and Risk Tolerance:

- Predictable Costs: If you prefer predictable monthly costs and a limit on annual out-of-pocket expenses, Medicare Advantage’s out-of-pocket maximum can offer peace of mind.

- Higher Monthly Premiums for Broader Coverage: If you’re willing to pay higher monthly premiums for Medigap and Part D to have the freedom to choose any Medicare-accepting provider and minimize your direct out-of-pocket costs at the point of service, Original Medicare with supplements might be your preference.

- Budget Constraints: If you’re on a tight budget, a $0 premium Medicare Advantage plan could be appealing, but be sure to understand the copayments and coinsurance for services.

3. Lifestyle and Travel Habits:

- Travelers: If you travel frequently within the U.S. or live in different states for parts of the year, Original Medicare offers greater flexibility as it’s accepted nationwide. Medicare Advantage plans often have service areas, and out-of-network care may be limited or more expensive.

- Local Care: If you primarily receive care from local doctors and hospitals and are comfortable with a network, a Medicare Advantage plan could be a good fit.

4. Access to Specific Doctors and Hospitals:

- Specific Providers: Do you have specific doctors or specialists you want to continue seeing? It’s crucial to confirm if they accept your chosen Medicare Advantage plan or if they accept Original Medicare.

- Referral Preference: Are you comfortable getting referrals from a primary care physician to see specialists, or do you prefer direct access?

5. Additional Benefits Desired:

- Do you value routine vision, dental, hearing, or fitness benefits? If so, Medicare Advantage plans often include these, saving you from purchasing separate plans. Original Medicare does not cover these.

The Enrollment Process for 2026

Regardless of whether you choose Original Medicare or Medicare Advantage, understanding the enrollment periods is vital. For Medicare 2026 Comparison, keep these dates in mind:

- Initial Enrollment Period (IEP): This is your first opportunity to enroll in Medicare. It’s a seven-month period that begins three months before your 65th birthday month, includes your birthday month, and extends three months after. If you don’t enroll during your IEP, you may face penalties or gaps in coverage.

- General Enrollment Period (GEP): If you miss your IEP and don’t qualify for a Special Enrollment Period, you can enroll in Part A and/or Part B during the GEP, which runs from January 1 to March 31 each year. Your coverage will begin the month after you enroll, and you may have to pay a late enrollment penalty.

- Annual Enrollment Period (AEP): From October 15 to December 7 each year, you can make changes to your Medicare coverage for the following year (2026). During this time, you can:

- Switch from Original Medicare to Medicare Advantage.

- Switch from Medicare Advantage to Original Medicare.

- Change Medicare Advantage plans.

- Change Part D prescription drug plans.

- Enroll in a Part D plan if you didn’t previously have one.

- Medicare Advantage Open Enrollment Period (MA OEP): From January 1 to March 31 each year, if you’re already in a Medicare Advantage plan, you can switch to a different Medicare Advantage plan or switch to Original Medicare (and join a separate Medicare Part D Plan).

- Special Enrollment Periods (SEPs): These periods allow you to make changes to your Medicare coverage outside of the standard enrollment periods due to certain life events, such as moving, losing other coverage, or qualifying for Extra Help.

It is important to mark these dates on your calendar as you conduct your Medicare 2026 Comparison research. Missing an enrollment period can lead to delayed coverage, late enrollment penalties, or being stuck in a plan that doesn’t meet your needs.

Conclusion: Your Informed Decision for Medicare 2026 Comparison

Choosing between Medicare Advantage and Original Medicare for 2026 is a significant decision that will impact your healthcare access and financial well-being. Both options offer robust coverage, but they do so through different structures, with distinct advantages and disadvantages. Original Medicare provides broad provider choice and the option to supplement with Medigap for reduced out-of-pocket costs, though it requires separate prescription drug coverage. Medicare Advantage offers an all-in-one approach with additional benefits, an out-of-pocket maximum, and often lower monthly premiums, but typically comes with network restrictions.

As you conduct your personal Medicare 2026 Comparison, take the time to honestly assess your health needs, financial situation, preferred healthcare providers, and travel habits. Utilize resources from Medicare.gov, consult with trusted insurance brokers specializing in Medicare, and speak with your healthcare providers about which plans they accept. The goal is to find a plan that not only covers your medical needs but also provides peace of mind and financial security.

Remember, the best plan for someone else might not be the best plan for you. Proactive research and a thorough understanding of the differences will empower you to make an informed decision for your health coverage in 2026 and beyond. By carefully weighing all the factors discussed in this guide, you can confidently navigate the complexities of Medicare and secure the healthcare coverage that’s right for you.