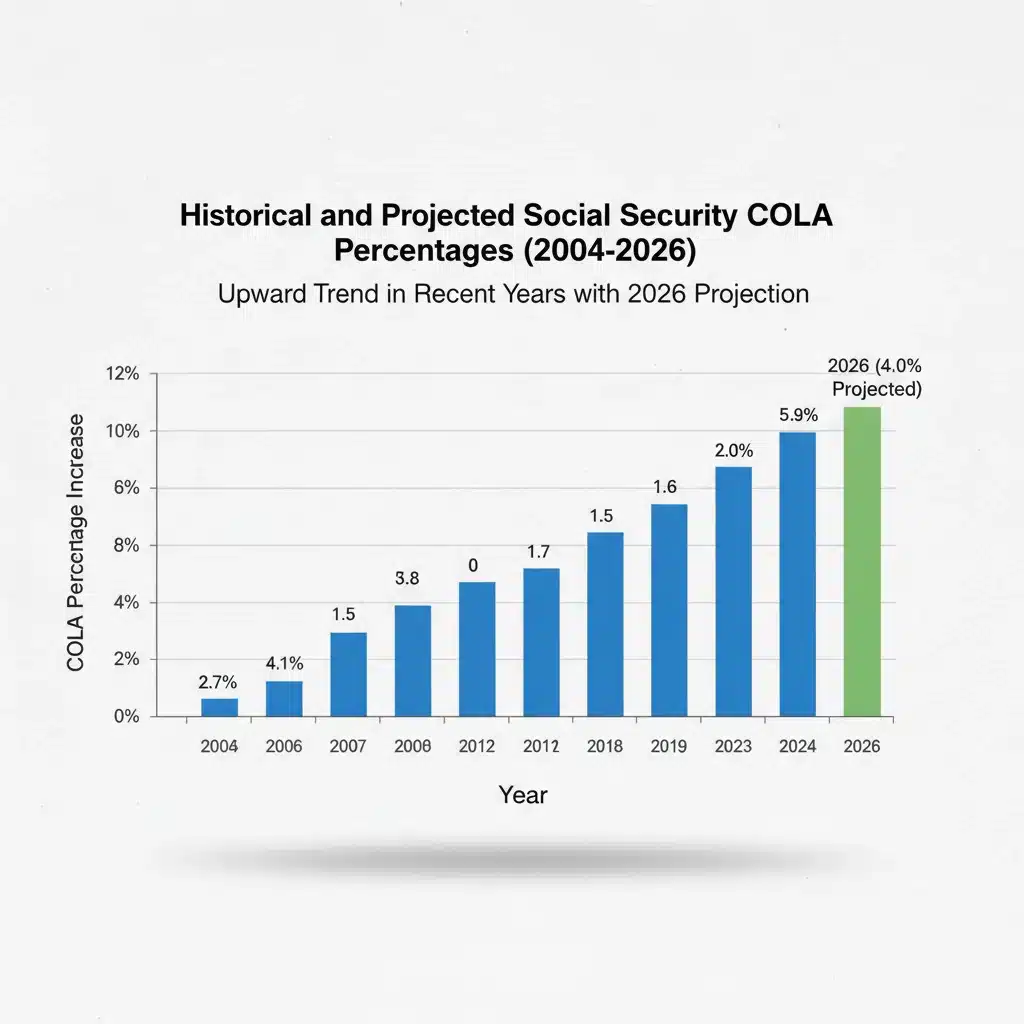

2026 Social Security COLA: What the 3.2% Adjustment Means for Your Retirement

Navigating the 2026 Social Security Benefit Adjustments: What the 3.2% COLA Means for Your Retirement Income

The financial landscape for retirees is constantly evolving, and one of the most critical factors influencing retirement income is the annual Social Security Cost-of-Living Adjustment (COLA). As we look ahead, projections suggest a significant Social Security COLA 2026 of 3.2%. This adjustment, while a projection, carries substantial weight for millions of Americans who rely on Social Security benefits to cover their living expenses. Understanding what this 3.2% COLA means, how it’s calculated, and its potential impact on your financial planning is crucial for securing a comfortable retirement.

For many, Social Security represents a foundational pillar of their retirement strategy. These benefits are designed to provide a safety net, protecting retirees, survivors, and disabled individuals from the brunt of inflation. The COLA mechanism is the primary tool used to achieve this protection. Without regular adjustments, the purchasing power of Social Security benefits would erode over time, leaving beneficiaries struggling to keep pace with rising costs. The anticipated Social Security COLA 2026 of 3.2% is a direct response to prevailing economic conditions, particularly inflation trends, and aims to ensure that benefits retain their real value.

The Mechanics of COLA: How the 3.2% for 2026 is Determined

To fully grasp the significance of the projected Social Security COLA 2026, it’s essential to understand the underlying methodology. The Cost-of-Living Adjustment is not an arbitrary figure; it’s a precise calculation mandated by law. The Social Security Administration (SSA) determines the COLA based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). Specifically, they compare the average CPI-W for the third quarter (July, August, and September) of the current year with the average CPI-W for the third quarter of the most recent year in which a COLA was enacted.

If the CPI-W has increased, the percentage increase becomes the COLA for the following year. If there’s no increase, or a decrease, there’s no COLA. This ensures that benefits do not fall behind the cost of living. The 3.2% projection for the Social Security COLA 2026 suggests that economists and analysts anticipate a continued, albeit potentially moderating, inflationary environment leading up to the calculation period. While the final figure won’t be announced until October 2025, these early projections provide valuable insights for forward-thinking retirees and financial planners.

It’s important to note that the CPI-W is a specific measure of inflation that tracks the spending habits of urban wage earners and clerical workers. Critics sometimes argue that this index doesn’t fully capture the spending patterns and healthcare costs of seniors, who often face unique inflationary pressures. However, it remains the legally mandated index for COLA calculations. Understanding this nuance helps in appreciating why the Social Security COLA 2026 might feel different for individual retirees based on their personal spending profiles.

The historical context of COLA adjustments also provides valuable perspective. Some years have seen modest increases, while others, particularly those following periods of high inflation, have witnessed more substantial adjustments. The projected 3.2% for the Social Security COLA 2026 falls within a range that suggests a continued effort to maintain benefit purchasing power without reaching the peak inflation levels seen in a few recent years. This balance is crucial for both beneficiaries and the long-term solvency of the Social Security program.

The Impact of a 3.2% COLA on Your Retirement Income

A 3.2% increase in your Social Security benefits can have a tangible effect on your monthly income. While it might seem like a modest percentage, over the course of a year, and especially over many years of retirement, these adjustments accumulate. For a retiree receiving an average monthly benefit, a 3.2% COLA translates into a noticeable boost, helping to offset the rising costs of everyday necessities such as groceries, utilities, and transportation. This is the core purpose of the Social Security COLA 2026 – to ensure that your fixed income doesn’t lose its value.

Consider an average monthly Social Security benefit. If that benefit is, for example, $1,800, a 3.2% increase would add $57.60 to your monthly check, totaling an additional $691.20 over the year. While this might not drastically change your lifestyle, it can be the difference between comfortably covering essential expenses or having to dip into savings. For those with lower fixed incomes, even small adjustments from the Social Security COLA 2026 can be critically important for maintaining financial stability.

Beyond the immediate financial boost, the COLA also plays a psychological role. Knowing that your primary source of retirement income is designed to keep pace with inflation provides a sense of security and reduces financial anxiety. This stability is invaluable for retirees, allowing them to plan their budgets with greater confidence. It reinforces the idea that Social Security is a reliable and adaptable program, designed to support beneficiaries through varying economic conditions.

However, it’s also crucial to consider the broader economic context. While the Social Security COLA 2026 aims to combat inflation, it doesn’t always perfectly align with every individual’s personal inflation rate. Factors like healthcare costs, which tend to rise faster than general inflation, can still put a strain on some retirees’ budgets. Therefore, while appreciating the benefit of the COLA, retirees should also maintain a holistic view of their financial health and explore other avenues for managing expenses and growing their retirement savings.

Beyond the Percentage: Understanding the Broader Economic Landscape

The projected 3.2% Social Security COLA 2026 doesn’t exist in a vacuum. It’s a reflection of and a response to the larger economic environment. Inflationary pressures, labor market conditions, and global economic trends all play a role in shaping the CPI-W and, consequently, the COLA. Understanding these broader forces can help retirees and future retirees anticipate future adjustments and plan accordingly.

Currently, many economies are navigating a period of elevated inflation, a trend that began in the wake of the COVID-19 pandemic and has been influenced by supply chain disruptions, geopolitical events, and strong consumer demand. While inflation may be moderating from its peaks, it remains a significant factor. The 3.2% projection for the Social Security COLA 2026 suggests that while price increases might not be as rapid as in some recent years, they are still substantial enough to warrant a meaningful adjustment to benefits. This indicates that the Federal Reserve’s efforts to control inflation are having an effect, but the battle is ongoing.

Another important consideration is the state of the labor market. A strong labor market, characterized by low unemployment and rising wages, can contribute to inflationary pressures as consumers have more disposable income. Conversely, a weakening labor market could lead to less consumer spending and potentially lower inflation. These dynamics indirectly influence the CPI-W and thus the Social Security COLA 2026. Staying informed about economic forecasts and central bank policies can provide valuable clues about potential future COLA trends.

Furthermore, global events, such as energy price fluctuations or international trade disputes, can ripple through the economy and affect domestic prices. For instance, a surge in global oil prices can directly impact transportation costs and utility bills, contributing to higher inflation. These complex interconnections highlight why a seemingly simple percentage like the 3.2% Social Security COLA 2026 is actually the outcome of numerous intricate economic factors at play on both national and international scales.

Financial Planning Strategies in Light of the 2026 COLA

Knowing about the projected Social Security COLA 2026 of 3.2% allows for proactive financial planning. While Social Security provides a vital baseline, it’s often not enough to cover all retirement expenses. Therefore, integrating this information into your broader financial strategy is key. Here are several strategies to consider:

- Re-evaluate Your Budget: With a potential increase in benefits, take the opportunity to review your current budget. See where the extra funds can be best allocated – perhaps to cover rising healthcare premiums, reduce debt, or even contribute to a modest savings goal. Even a small increase from the Social Security COLA 2026 can provide a buffer.

- Consider Healthcare Costs: As mentioned, healthcare costs often outpace general inflation. Factor in these rising expenses when budgeting, and explore options like Medicare Advantage plans or supplemental insurance to manage out-of-pocket costs. The COLA might help, but it’s unlikely to cover all healthcare inflation.

- Diversify Income Streams: Relying solely on Social Security can be risky. Explore ways to diversify your retirement income, such as drawing from investment portfolios, pensions, or even part-time work. This multi-faceted approach provides greater financial resilience, especially when the Social Security COLA 2026 might not fully cover all your needs.

- Consult a Financial Advisor: A professional financial advisor can help you integrate the projected COLA into your long-term retirement plan. They can provide personalized advice on investment strategies, tax implications, and overall wealth management, taking into account your specific financial situation and goals. Understanding how the Social Security COLA 2026 fits into your bigger picture is crucial.

- Monitor Inflation Trends: Keep an eye on economic news and inflation reports. While the COLA is an annual adjustment, understanding ongoing economic trends can help you anticipate future adjustments and make timely financial decisions. This proactive approach can help you stay ahead of the curve.

- Optimize Your Social Security Claiming Strategy: If you haven’t started receiving benefits yet, understanding how COLA affects delayed claiming strategies is important. Delaying benefits can lead to higher monthly payments, which are then subject to COLA increases, potentially amplifying the benefit of the Social Security COLA 2026 and future adjustments.

By taking these steps, you can ensure that the Social Security COLA 2026 effectively contributes to your financial well-being, rather than merely keeping your head above water. Proactive planning is always the best defense against economic uncertainties.

The Long-Term Outlook for Social Security and Future COLAs

While the 3.2% Social Security COLA 2026 is a welcome projection, it’s also important to consider the long-term outlook for the Social Security program itself. The program faces ongoing solvency challenges, primarily due to demographic shifts – a growing number of retirees relative to the working population. These challenges often lead to discussions about potential reforms, which could impact future benefit levels and COLA mechanisms.

The Social Security Administration regularly releases trustee reports that project the program’s financial health decades into the future. These reports often highlight the need for legislative action to ensure the program’s long-term sustainability. Potential reforms could include adjustments to the full retirement age, changes to the benefit calculation formula, or modifications to the COLA calculation method itself. While these are complex political and economic discussions, they are critical for anyone relying on Social Security benefits.

For current retirees, these long-term discussions might seem distant, but they underscore the importance of not relying solely on Social Security. For those still working, understanding these potential future changes can inform their retirement savings strategies, encouraging greater personal responsibility and diversification of retirement assets. The Social Security COLA 2026 is a snapshot of the program’s adaptability, but its future stability depends on broader policy decisions.

Another aspect to consider is the potential for different inflation measures to be used for COLA calculations in the future. The Chained CPI, for example, is sometimes proposed as an alternative to the CPI-W. The Chained CPI generally shows lower inflation rates because it accounts for consumers substituting cheaper goods when prices rise. If such a change were enacted, it could lead to smaller COLAs in the future, thus altering the impact of subsequent adjustments compared to the projected Social Security COLA 2026.

Staying informed about these ongoing debates and potential legislative changes is part of comprehensive retirement planning. While the immediate outlook with the Social Security COLA 2026 is positive, a forward-looking perspective is always beneficial.

Maximizing Your Social Security Benefits Beyond COLA

While the Social Security COLA 2026 helps maintain the purchasing power of your benefits, there are other strategies you can employ to maximize your overall Social Security income. These strategies primarily revolve around when and how you claim your benefits.

- Delaying Benefits: For every year you delay claiming Social Security benefits past your full retirement age (up to age 70), your benefit amount increases by a certain percentage, known as Delayed Retirement Credits. These credits can significantly boost your monthly payment. For example, if your full retirement age is 67, and you delay claiming until 70, your monthly benefit could be 24% higher. This higher starting amount is then subject to annual COLA adjustments, including the Social Security COLA 2026, leading to even larger future increases.

- Understanding Spousal Benefits: If you are married, divorced (under certain conditions), or widowed, you may be eligible for spousal or survivor benefits. These can sometimes be higher than your own earned benefit, particularly if your spouse had a much higher earning history. Understanding these rules can help you coordinate claiming strategies with your spouse to maximize your household’s total Social Security income, which will then be impacted by the Social Security COLA 2026.

- Working in Retirement: Continuing to work, even part-time, in retirement can have several benefits. It can reduce the amount you need to draw from your Social Security benefits, allowing them to grow further if you haven’t claimed yet. Additionally, if your current earnings are higher than some of your past earnings, your Social Security benefit could be recalculated to reflect these higher-earning years, potentially increasing your base benefit before any COLA, including the Social Security COLA 2026, is applied.

- Reviewing Your Earnings Record: Regularly check your Social Security earnings record for accuracy. Mistakes can happen, and incorrect information could lead to lower benefits. You can access your earnings record through your my Social Security account online. Ensuring your record is accurate is a fundamental step in maximizing your benefits, which will then be correctly adjusted by the Social Security COLA 2026.

- Tax Implications: A portion of Social Security benefits may be taxable depending on your combined income. Understanding these thresholds and planning your other retirement income withdrawals strategically can help minimize your tax burden, effectively increasing the net value of your Social Security income, including the boost from the Social Security COLA 2026.

By implementing these strategies, you can not only benefit from the annual Social Security COLA 2026 but also enhance your overall financial security in retirement. It’s about being strategic and informed about all aspects of your Social Security benefits.

Conclusion: Preparing for the 2026 Social Security COLA and Beyond

The projected 3.2% Social Security COLA 2026 is an important piece of news for current and future retirees. It represents the Social Security Administration’s ongoing commitment to ensuring that benefits maintain their purchasing power in the face of inflation. While the final figure is still subject to the official calculation in late 2025, this projection provides a valuable benchmark for financial planning.

Understanding how the COLA is calculated, its direct impact on your monthly income, and the broader economic forces at play allows you to make more informed decisions about your retirement finances. It’s a reminder that while Social Security is a robust program, it’s most effective when integrated into a comprehensive retirement strategy that includes diversified income streams, careful budgeting, and proactive management of healthcare costs.

As you look ahead to the Social Security COLA 2026 and beyond, remember that staying informed is your best asset. Monitor economic news, review your financial plan regularly, and don’t hesitate to seek professional advice. By taking these steps, you can navigate the complexities of retirement income with confidence, ensuring that you are well-prepared for any adjustments and changes that the future may hold. The goal is not just to receive a COLA, but to leverage it as part of a secure and comfortable retirement.