Mastering FAFSA 2026-2027: Your Guide to Federal Student Aid

Mastering FAFSA 2026-2027: Your Comprehensive Guide to Federal Student Aid

Navigating the world of federal student aid can often feel like deciphering a complex code. For the 2026-2027 academic year, understanding the Free Application for Federal Student Aid (FAFSA) is more crucial than ever. With ongoing changes and updates to the application process, staying informed is the first step toward unlocking the financial assistance you need for higher education. This comprehensive guide is designed to demystify the FAFSA 2026-2027 Guide, providing you with a step-by-step roadmap to ensure you maximize your eligibility for grants, scholarships, work-study programs, and federal student loans.

The FAFSA is more than just a form; it’s your gateway to billions of dollars in federal financial aid. Many states and colleges also use your FAFSA information to determine eligibility for their own aid programs. Therefore, understanding its nuances and completing it accurately and on time is paramount. This article will walk you through everything you need to know, from the critical changes introduced in recent years to the essential documents required and expert tips for a smooth application process. Get ready to master the FAFSA and secure your educational future.

Understanding the FAFSA: What is it and Why is it Important for 2026-2027?

The FAFSA, or Free Application for Federal Student Aid, is a form completed by current and prospective college students in the United States to determine their eligibility for student financial aid. This aid can come from various sources, including the federal government, state governments, and individual colleges and universities. For the 2026-2027 academic year, the FAFSA remains the cornerstone of financial aid applications, but it’s essential to acknowledge the significant changes that have been implemented in recent cycles, particularly those stemming from the FAFSA Simplification Act.

The importance of completing the FAFSA cannot be overstated. Without it, you are automatically ineligible for federal grants like the Pell Grant, federal student loans, and federal work-study programs. Furthermore, many state-specific aid programs and institutional scholarships require a completed FAFSA to assess your financial need. Even if you believe your family earns too much money to qualify for aid, it’s always advisable to complete the FAFSA. Many forms of aid are not need-based, and unexpected circumstances can sometimes qualify families for assistance they didn’t anticipate.

The 2026-2027 FAFSA will utilize financial information from the 2024 tax year. This ‘prior-prior year’ system means you won’t need to wait until your 2025 taxes are filed to complete the application, allowing for earlier submission and, potentially, earlier aid offers. This early submission is critical because some aid is awarded on a first-come, first-served basis, and state and institutional deadlines can be quite early.

Key Changes and Updates Affecting the FAFSA 2026-2027

The FAFSA Simplification Act has brought about monumental changes, and while many were implemented for the 2024-2025 cycle, their impact will continue to be felt and refined for the 2026-2027 FAFSA. Understanding these changes is vital for a successful application.

- Simplified Form: The FAFSA has been significantly streamlined, reducing the number of questions. This aims to make the application process quicker and less daunting for families.

- New Terminology: Familiar terms like ‘Expected Family Contribution’ (EFC) have been replaced with the ‘Student Aid Index’ (SAI). The SAI is a new eligibility index that determines federal student aid. A lower SAI indicates a greater financial need.

- Direct Data Exchange (DDX) with IRS: This is a major change. Applicants (and their contributors, if applicable) will be required to provide consent for the IRS to directly share their tax data with the Department of Education. This mandatory consent simplifies data entry, reduces errors, and makes the process more secure. Without this consent, applicants will not be eligible for federal student aid.

- Expanded Pell Grant Eligibility: The new methodology for calculating the SAI aims to expand Pell Grant eligibility to more students and ensure that more students with the greatest need receive the maximum Pell Grant award.

- Changes to Family Size: The definition of ‘family size’ (previously household size) will now align with the number of individuals reported on the tax return. This could impact the SAI calculation for some families.

- Treatment of Small Businesses and Farms: For families who own a small business or farm, the net worth of these assets, which previously might have been excluded, will now be included in the asset calculation, potentially affecting eligibility for some.

- Child Support: Child support received will now count as an asset, not as untaxed income. This change could also impact the SAI.

- Multiple Children in College: The previous benefit of having multiple children in college simultaneously, which reduced the EFC for each student, has been eliminated. The SAI will no longer divide by the number of students in college, which could lead to a higher SAI for families with multiple children pursuing higher education concurrently.

These changes are designed to create a more equitable and efficient aid system. However, they also mean that families who were previously accustomed to the old FAFSA process will need to pay close attention to the new requirements and calculations. Familiarizing yourself with these updates now will save you time and potential headaches when the 2026-2027 FAFSA becomes available.

Who Should Apply for FAFSA 2026-2027? Eligibility Criteria Explained

Understanding who is eligible to apply for federal student aid is fundamental. While the FAFSA Simplification Act has brought changes to how aid is calculated, the basic eligibility requirements for federal student aid remain largely consistent. Most U.S. citizens and eligible non-citizens who demonstrate financial need and meet certain academic requirements are eligible.

General Eligibility Requirements:

- U.S. Citizen or Eligible Non-Citizen: This includes U.S. nationals, permanent residents (green card holders), and those with an Arrival-Departure Record (I-94) showing refugee, asylum granted, or parolee status, among others.

- Valid Social Security Number (SSN): With some exceptions for citizens of the Freely Associated States.

- High School Diploma or GED: Or completion of a state-recognized homeschooling program.

- Enrolled or Accepted for Enrollment: In an eligible degree or certificate program at an eligible institution.

- Maintain Satisfactory Academic Progress (SAP): As defined by the college or university you attend.

- Sign Statements of Educational Purpose and Certification Statement: Confirming you will use federal student aid only for educational purposes and are not in default on any federal student loan, nor do you owe a refund on a federal student grant.

- Not Be Incarcerated: While incarcerated individuals may have limited eligibility for Pell Grants, specific federal student loans are generally not available.

Dependency Status:

A critical aspect of the FAFSA is determining whether you are considered a ‘dependent’ or ‘independent’ student. This status dictates whose information needs to be reported on the FAFSA. If you are a dependent student, you must report your parents’ information. If you are independent, you only report your own (and your spouse’s, if applicable) information.

You are generally considered an independent student if you meet one or more of the following criteria:

- You are 24 years old or older by December 31 of the award year.

- You are married.

- You are working on a master’s or doctorate degree.

- You have children or other dependents who receive more than half of their support from you.

- You are currently serving on active duty in the U.S. Armed Forces or are a veteran.

- You are an orphan (both parents deceased), a ward of the court, or were in foster care at any time after age 13.

- You are an emancipated minor or are in a legal guardianship.

- You are homeless or at risk of being homeless.

If you do not meet any of these criteria, you are considered a dependent student for FAFSA purposes, regardless of whether your parents claim you on their tax return or if you live with them. Understanding your dependency status early will help you gather the correct information and avoid delays.

Required Documents for the FAFSA 2026-2027 Application

Gathering all necessary documents before you begin the FAFSA application is crucial for a smooth and efficient process. Since the 2026-2027 FAFSA will use your 2024 tax information, start compiling those records now. Although the Direct Data Exchange (DDX) simplifies the transfer of IRS tax data, having your documents handy will help you review the information and answer any non-tax-related questions accurately.

Documents for Students:

- Your Social Security Number (SSN): Ensure it is correct.

- Your Alien Registration Number (A-Number): If you are an eligible non-citizen.

- Your 2024 Federal Income Tax Returns: Though the DDX will pull this, having your W-2s, 1099s, and complete tax return (e.g., Form 1040) for reference is wise.

- Records of Other Income: Any untaxed income received in 2024, such as child support received (now counted as an asset), interest income, and veterans’ non-education benefits.

- Records of Your Assets: Information about your cash, savings, checking account balances, investments (e.g., stocks, bonds, mutual funds, 529 plans), and real estate (excluding the home you live in) as of the day you complete the FAFSA.

- List of Colleges You Are Interested In: You can list up to 20 schools on the online FAFSA.

Documents for Parents (if you are a dependent student):

- Parents’ Social Security Numbers (SSNs): For all parents whose information is required.

- Parents’ 2024 Federal Income Tax Returns: W-2s, 1099s, and complete tax return (e.g., Form 1040). Again, the DDX will be used, but reference documents are helpful.

- Parents’ Records of Other Income: Untaxed income received in 2024.

- Parents’ Records of Assets: Cash, savings, checking account balances, investments, and real estate (excluding the family home) as of the day you complete the FAFSA. This now includes net worth of small businesses and farms.

It’s important to note that if your parents are divorced or separated, the parent whose financial information is required on the FAFSA is the one who provided more financial support to you during the 12 months prior to filing the FAFSA. If that parent has remarried, their spouse’s information (your stepparent) must also be included.

Having these documents organized and readily available will significantly speed up the application process and reduce the likelihood of errors, which could delay your financial aid award.

Step-by-Step Guide to Completing the FAFSA 2026-2027 Online

The online FAFSA application is the most efficient way to apply. Follow these steps to ensure a successful submission for the 2026-2027 academic year:

Step 1: Create an FSA ID (Federal Student Aid ID)

Both the student and at least one parent (if the student is dependent) need an FSA ID. This is a username and password combination that serves as your electronic signature and provides access to federal student aid websites. If you already have one, ensure it’s active and you remember your credentials. If not, create one at studentaid.gov. It can take 1-3 days for the FSA ID to become active, so do this well in advance.

Step 2: Gather Required Documents

As detailed in the previous section, collect all necessary documents for yourself and your parents (if applicable) before you start. This includes SSNs, tax returns (2024 for 2026-2027 FAFSA), and asset information.

Step 3: Access the FAFSA Online Application

Once the 2026-2027 FAFSA becomes available (typically October 1st, though recent changes have shifted this for some cycles, always check the official studentaid.gov website for the exact launch date), go to studentaid.gov and click ‘Start New FAFSA’.

Step 4: Complete the Student Demographics Section

You’ll begin by entering your personal information, such as your name, date of birth, address, and citizenship status. This section also includes questions to determine your dependency status.

Step 5: Provide Consent for IRS Direct Data Exchange (DDX)

This is a critical new step. Both the student and any required contributors (parents, spouse) must provide consent for the IRS to directly share their tax information with the Department of Education. This consent is mandatory for federal student aid eligibility. The FAFSA form will guide you through this process, which involves logging into your FSA ID and authorizing the data transfer.

Step 6: Enter Financial Information (if not fully covered by DDX)

While the DDX will import most tax data, you may still need to manually enter information about your assets (cash, savings, investments) and any untaxed income not reported on a tax return. Be precise and update asset values to the date you are completing the FAFSA.

Step 7: List Schools You Want to Receive Your FAFSA Information

Add the Federal School Codes for all colleges and universities you are considering. You can list up to 20 schools online. Each school will receive your FAFSA data and use it to determine your eligibility for institutional aid.

Step 8: Review and Sign Your FAFSA

Carefully review all sections of your FAFSA for accuracy. Any errors could delay processing or affect your aid eligibility. Once reviewed, electronically sign your FAFSA using your FSA ID. If you are a dependent student, your parent(s) will also need to log in with their FSA ID to provide their consent for DDX and electronically sign the application.

Step 9: Submit Your FAFSA

After signing, submit your application. You will receive a confirmation page with a confirmation number. Save this for your records.

Step 10: What Happens Next?

Within a few days to weeks, you will receive a FAFSA Submission Summary (FSS), which replaces the old Student Aid Report (SAR). This document summarizes the information you submitted and includes your Student Aid Index (SAI). Review it carefully for any errors. If you find mistakes, you can log back into your FAFSA and make corrections. Colleges will use your FAFSA data to create financial aid packages, which they will send to you directly.

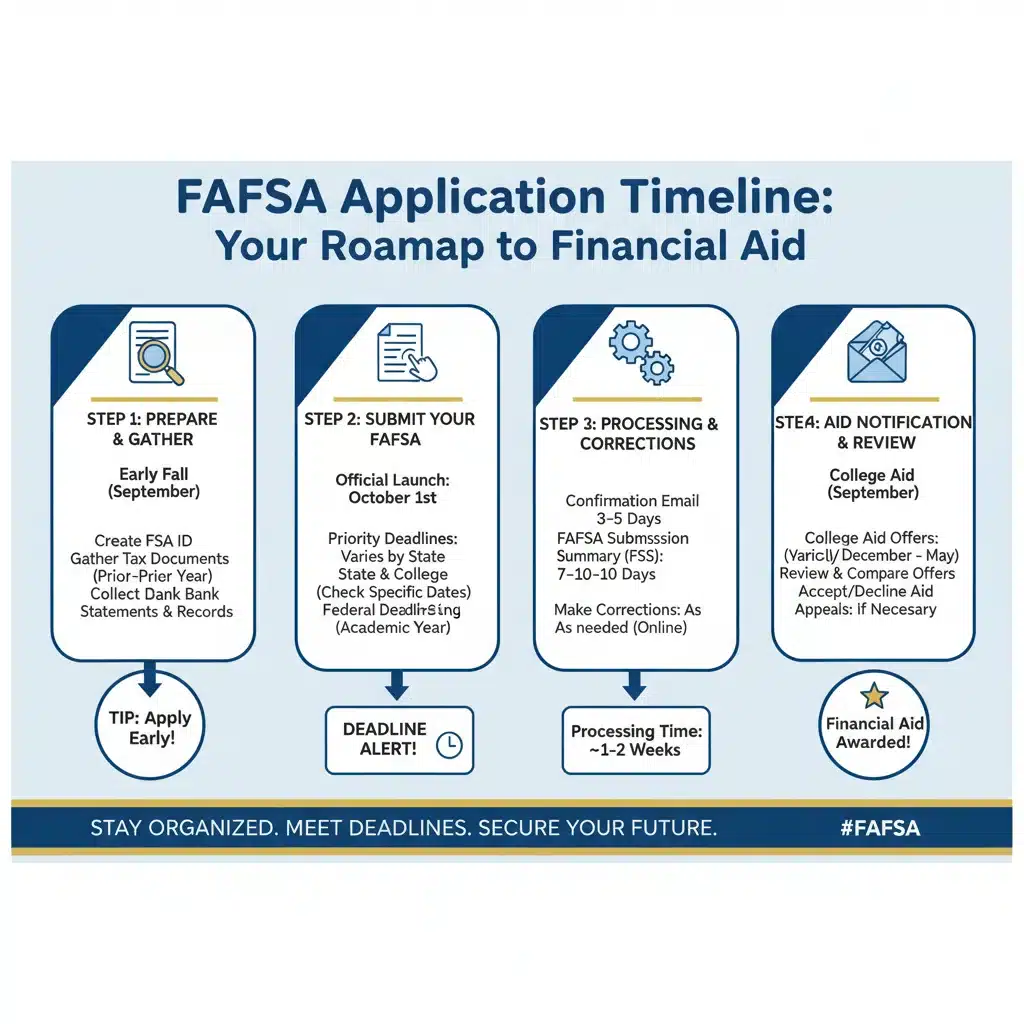

Key Dates and Deadlines for FAFSA 2026-2027

Meeting deadlines is paramount when it comes to federal student aid. Missing a deadline can mean losing out on valuable financial assistance. While federal deadlines are consistent, state and institutional deadlines can vary significantly.

Federal FAFSA Deadline: The federal deadline for the 2026-2027 FAFSA is typically June 30, 2027. However, this is largely for federal Pell Grants and federal loans. Many other forms of aid are awarded on a first-come, first-served basis, making early submission critical.

State FAFSA Deadlines: Each state has its own deadline for state-funded financial aid programs. These deadlines can be as early as January or February of the year you plan to attend college. It is essential to check your specific state’s deadline on the Federal Student Aid website or your state’s higher education agency website.

College FAFSA Deadlines: Individual colleges and universities also have their own deadlines, especially for institutional grants and scholarships. These can often be the earliest deadlines you face. Check the financial aid website of each school you are applying to for their specific FAFSA submission deadlines and any other required forms.

General Timeline for the FAFSA 2026-2027:

- Fall 2025 (October 1st is the traditional opening date, but always verify for 2026-2027): The 2026-2027 FAFSA becomes available. This is the ideal time to complete and submit your application.

- Winter 2025 – Spring 2026: Continue to submit your FAFSA if you haven’t already. Pay close attention to state and institutional deadlines, which often fall within this period.

- Spring – Summer 2026: Colleges begin to send out financial aid offer letters. Review these carefully and compare offers from different schools.

- June 30, 2027: Federal FAFSA deadline for the 2026-2027 academic year.

Pro Tip: Aim to submit your FAFSA as close to the opening date as possible. This ensures you are considered for all available aid, especially state and institutional grants that may have limited funding.

Maximizing Your Federal Student Aid: Tips and Strategies

Completing the FAFSA accurately and on time is a great start, but there are additional strategies you can employ to potentially maximize the federal student aid you receive.

1. Submit Early, Every Year:

This cannot be stressed enough. Some financial aid, particularly state and institutional grants, operates on a first-come, first-served basis. Submitting your FAFSA as soon as it opens (typically October 1st, though recent years have seen shifts) puts you in the best position to receive these funds. Remember to reapply every year you plan to attend college.

2. Be Accurate and Honest:

Provide precise information. Even small errors can lead to delays or incorrect aid calculations. The DDX will help with tax data, but double-check all manually entered information, especially asset values. Deliberately misrepresenting information can lead to serious consequences, including fines or imprisonment.

3. Understand the Student Aid Index (SAI):

The SAI replaces the EFC. A lower SAI indicates more financial need. While you can’t drastically change your family’s income, understanding how assets are treated (e.g., retirement accounts are not counted, certain savings plans are) can help in financial planning. Note the new treatment of small businesses/farms and child support received.

4. Don’t Assume You Won’t Qualify:

Many families mistakenly believe they earn too much money to qualify for financial aid. However, there’s no income cut-off for federal student aid. Factors like family size, number of children in college, and specific college costs all play a role. Plus, the FAFSA is essential for federal student loans, which are often available regardless of income.

5. Report Special Circumstances:

If your family has experienced a significant financial change since the 2024 tax year (e.g., job loss, divorce, death of a parent, high medical expenses not covered by insurance), contact the financial aid office at your prospective colleges. They have the discretion to make adjustments to your FAFSA data, a process known as ‘professional judgment’, which could increase your aid eligibility.

6. Compare Financial Aid Offers:

Once you receive financial aid offer letters from different schools, compare them carefully. Look beyond the sticker price and focus on the ‘net price’ – the cost remaining after grants and scholarships are applied. Understand the difference between grants (free money), work-study (earned money), and loans (money that must be repaid).

7. Explore State and Institutional Aid Beyond FAFSA:

While FAFSA is foundational, many states and colleges have their own applications for aid. Check with your state’s higher education agency and each college’s financial aid office for specific requirements and additional forms, such as the CSS Profile.

8. Keep Good Records:

Maintain copies of all documents used to complete your FAFSA, your FAFSA Submission Summary, and any correspondence from the Department of Education or colleges. This will be invaluable if you need to make corrections or appeal an aid decision.

9. Be Aware of Scams:

The FAFSA is free. You should never pay to complete or submit the FAFSA. Be wary of any services that charge a fee to help you with the application. Stick to the official studentaid.gov website.

10. Use the FAFSA Help Resources:

The Federal Student Aid website offers extensive help, including online chat, email support, and a toll-free helpline. Don’t hesitate to use these resources if you encounter difficulties or have questions during the application process.

Common FAFSA Mistakes to Avoid for 2026-2027

Even with the simplified FAFSA, mistakes can happen. Being aware of common pitfalls can help you avoid them and ensure a smooth application process.

- Not Creating an FSA ID in Advance: This is a frequent delay. The FSA ID takes a few days to become active. Create it well before you plan to fill out the FAFSA.

- Missing Deadlines: As previously emphasized, state and institutional deadlines can be much earlier than the federal deadline. Mark all relevant deadlines on your calendar.

- Incorrectly Reporting Dependency Status: This is a common error. Review the dependency questions carefully. If you’re unsure, use the official FAFSA guidance.

- Forgetting to Include Consent for IRS DDX: This is a new, mandatory step. Without consent from all required contributors, your application will not be processed for federal aid.

- Reporting Current Year Income Instead of Prior-Prior Year: For 2026-2027, you must use 2024 tax information. Using 2025 or current income is incorrect.

- Errors in Social Security Numbers or Dates of Birth: These seemingly small errors can prevent your FAFSA from matching with other records, causing significant delays. Double-check all personal identifying information.

- Not Listing Enough Schools: You can list up to 20 schools. It’s wise to include all potential colleges you’re considering, even if you’re not sure you’ll apply to all of them. You can always add or remove schools later.

- Not Saving Your FAFSA Submission Summary (FSS): This document contains crucial information, including your SAI. Keep it accessible for future reference.

- Not Following Up: Check your FAFSA status periodically on studentaid.gov. Respond promptly to any requests for additional information from the Department of Education or your colleges.

- Not Understanding the Financial Aid Offer: Don’t just look at the total aid. Differentiate between grants, scholarships, work-study, and loans. Understand the terms and conditions of each.

By being meticulous and informed, you can steer clear of these common errors and facilitate a smoother journey through the FAFSA application for the 2026-2027 academic year.

Appealing a Financial Aid Decision or Reporting Special Circumstances

What if your financial aid offer doesn’t seem to reflect your family’s current financial situation? Or what if you encounter unforeseen circumstances after submitting your FAFSA? Don’t despair. You have options to appeal a financial aid decision or report special circumstances to your college’s financial aid office.

What are Special Circumstances?

Special circumstances are financial situations that differ from what is reflected on your 2024 tax return (the ‘prior-prior year’ data used for the 2026-2027 FAFSA). These can include:

- Loss of a job or significant reduction in income for a student or parent.

- Separation or divorce of parents after the FAFSA was filed.

- Death of a parent or spouse.

- Unusually high medical or dental expenses not covered by insurance.

- Elementary or secondary school tuition expenses.

- One-time income that inflated the prior-prior year’s income (e.g., severance pay).

- Changes in student dependency status due to an unsafe home environment.

The Professional Judgment Process:

Financial aid administrators have the authority, known as ‘professional judgment’, to adjust data elements on your FAFSA or even your dependency status if they determine that your circumstances warrant it. This can lead to a recalculation of your Student Aid Index (SAI) and potentially an increase in your aid eligibility.

How to Appeal or Report Special Circumstances:

- Contact the Financial Aid Office: As soon as you identify a special circumstance, reach out to the financial aid office at each college you are considering. Do not contact the Department of Education.

- Explain Your Situation Clearly: Be prepared to explain your circumstances in detail. Many colleges have a specific form or process for professional judgment requests.

- Provide Documentation: You will need to provide documentation to support your claim. This could include:

- Termination letters or unemployment benefit statements.

- Medical bills and insurance statements.

- Divorce decrees or legal separation documents.

- Death certificates.

- Letters from school counselors or social workers regarding dependency status.

- Be Persistent and Patient: The review process can take time. Follow up politely if you don’t hear back within a reasonable period.

Remember, each financial aid office has its own policies and procedures for handling special circumstances. What one school approves, another may not. It’s crucial to engage directly with the colleges you are interested in and provide all requested information promptly.

Conclusion: Your Path to Federal Student Aid for 2026-2027

The journey to higher education is an investment, and securing financial aid through the FAFSA 2026-2027 Guide is a critical step in making that investment manageable. While the FAFSA has undergone significant changes, the core principle remains the same: it’s your primary tool for accessing federal, state, and institutional financial assistance.

By understanding the new terminology, embracing the Direct Data Exchange, diligently gathering your documents, and submitting your application early, you position yourself for success. Don’t let the complexity deter you; break down the process into manageable steps, utilize available resources, and remember that financial aid offices are there to help.

Completing the FAFSA is an annual commitment, but one that pays dividends in reducing the financial burden of college. Take control of your educational funding by mastering the FAFSA 2026-2027. Your future self will thank you for the effort you put in today.